Our journey takes us through the crucial developments in the first half of the nineteenth century (when accountancy starts to take form as an organised profession growing primarily as a result of the commercial and legal activity of bankruptcy, insolvency and the winding up of companies) and takes us all the way to the present.

The beginning. Early printed works. Introduction of double-entry book-keeping to the UK. The first accountancy firm is established in Bristol.

The founder bodies and local societies emerge. Accountancy takes form as an organised profession. Early Legislation. A Royal Charter is granted.

Early organisation of the ICAEW. Setting the standards of professional conduct. Chartered Accountant's Hall is built. The question of the admission of women is raised.

First World War. The first women are admitted to the profession. Chartered Accountant's Hall is extended. 50th Anniversary of the ICAEW. The question of registration. The Royal Mail Fraud Trial.

Second World War. Courses for returning servicemen. Non-practising members gain influence within the Institute. The first Member's Handbook is published. Chartered Accountant's Hall is extended.

Attempts to restructure the profession. Co-operation between accountancy bodies is established. ICAEW Centenary. Enron and the collapse of US Andersen. Adoption of International Accounting Standards.

This timeline has primarily focused on the CCAB bodies/recognised qualifying bodies but there have been a number of other bodies in existence during the period covered. You can trace the development of these bodies through the Index of UK and Irish Accountancy and Professional Bodies.

To suggest additions or improvements to the timeline please contact the Library & Information Service at library@icaew.com

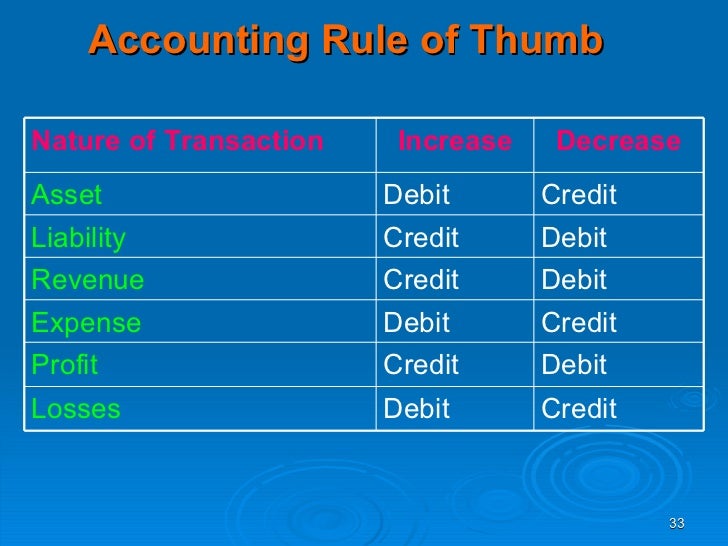

Debit and Credit

Debit and Credit are two actions of opposing nature that are relevant to the process of accounting.

Debiting an account and crediting an account are the two actions that are the result of an accounting transaction. We either debit an account or credit an account in relation to an accounting transaction but not both.

They are as fundamental to accounting as addition (+) and subtraction (−) are to mathematics. Trying to apply this mathematical analogy in all cases would give a distorted meaning. It would not be appropriate to consider debit to be an equivalent of addition and credit to be an equivalent of subtraction or vice versa.

We just need to understand that debit and credit are two actions that are opposite in nature.

An element (account head) that is effected by an accounting transaction is either debited or credited, with an amount that is reflected in the transaction, depending on the nature of the account and the rule applicable to it.

- A purchase of Furniture worth 10,000 for Cash.This transaction would result in

- Furniture a/c being debited by an amount of 10,000 and

- Cash a/c being credited by a similar amount.

- A payment of 5,000 received from Mr. Narayan by Cheque.This transaction would result in

- Mr. Narayan a/c being credited to the extent of 5,000 and

- The Bank a/c being debited with a similar amount.

Rules/Principles of Debit and Credit

The total process of accounting is driven by

- The dual entity concept

- The nature of the accounts and

- The rules/principles of debit and credit

All the account heads used in the accounting system of an organisation are classified under one of the three heads Real, Personal and Nominal. Each account type, has a pair of principles or rules of debit and credit relevant to it. One for debit and another for Credit.

No hay comentarios:

Publicar un comentario